Wednesday, March 4, 2026: At first glance, the Indian startups ecosystem seems to have hit a gold mine in February 2026. With a total venture capital inflow of $1.4 billion, the month recorded a staggering 110% year-on-year surge compared to the $669 million raised in February 2025. Even compared to January 2026, the ecosystem saw a 52% jump in capital deployment.

However, a look beneath the surface reveals a narrative of “the many and the one.”

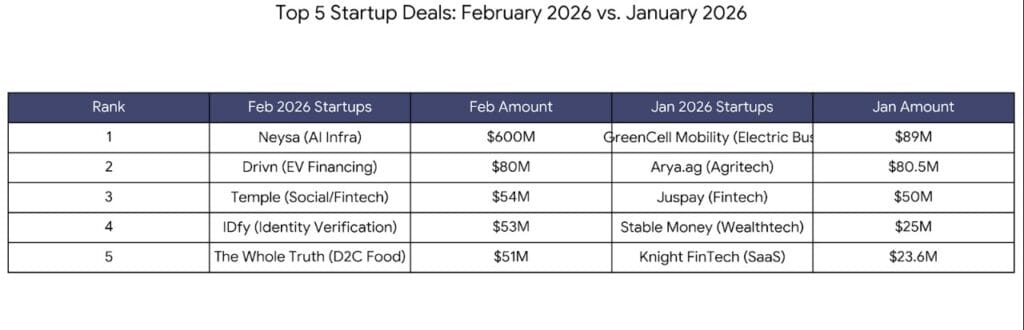

The headline growth is almost entirely the result of a single, massive transaction: Neysa’s $600 million mega-round. Without this outlier, the ecosystem’s performance paints a far more sober picture. Stripping away the Neysa deal, total funding would have hovered between $800 million and $900 million—a range that industry experts categorize as “average” at best.

The Indian Startups VC inflow data suggests that the broader funding momentum has yet to actually pick up. In fact, outside of Neysa, the month was notably devoid of “centurion” deals (transactions over $100 million). The top-tier activity was instead defined by mid-sized rounds, including Drivn ($80 million), IDfy ($53 million), Temple ($54 million), and The Whole Truth ($51 million).

Neysa’s Giant Leap Masks Steady Ground for Indian Startups in February

- The Neysa Effect: A single $600M deal accounted for nearly 43% of the month’s total capital.

- The Missing Middle: Zero deals exceeded the $100M mark outside of the AI sector leader.

- Resilient Early-Stage: Despite the capital crunch, over 100 deals were inked, signaling that the entrepreneurial spirit remains undeterred.

- Stage Trends: Growth-stage startups bagged the most capital, followed by early and late stages. Debt remained a minor player at $83 million.

- Sector Shakeup: AI and Cleantech outperformed Fintech, which historically dominates the charts.

- The Big Three Dominance: Mumbai, Bengaluru, and Delhi-NCR continues to corner over 90% of all funding.

A Shifting Sector Landscape

The most surprising shift this month in the Indian Startups funding ecosystem was in the sectoral hierarchy. Artificial Intelligence (AI) reigned supreme, reflecting a global investor appetite for localized LLMs and AI infrastructure. Cleantech and Direct-to-Consumer (D2C) followed closely. Remarkably, Fintech,usually the undisputed king of Indian VC—slipped to a modest fourth place.

Geographically, the map remains lopsided. Mumbai took the crown for the highest inflow, followed by Bengaluru and Delhi-NCR. While these hubs thrive, secondary cities like Chennai, Hyderabad, and Pune continue to struggle to match the capital magnetism of the “Big Three.”

The Road Ahead: H1 2026

The outlook for the remainder of the first half of the year remains cautious. With macroeconomic headwinds and escalating tensions in the Middle East, VCs are expected to remain selective.

While the high volume of deals (100+) proves that the pipeline of innovation is full, the “funding winter” hasn’t quite thawed, it’s just being kept warm by a few very large fires in the AI space.